Having to make all transfers manually through checks or going physically to pay utility bills can be a hassle in the city’s fast-paced daily lives. This can be especially true if you own a business. Merchants have to send and receive payments to and from multiple entities, and some of them are recurring payments that have to be paid at the end of each month. ACH payments are more common than an average person may think. Many people are already involved in ACH transactions and are entirely unaware of it. An excellent example of ACH transfers is that most Americans receive their salary each month. It is automatically deposited in their accounts without fail each time. ACH processing works in various ways, from ensuring the security of the payments to timely recurring payments. ACH transactions can be much more efficient than writing checks and can be more cost-effective than paying with a credit or debit card.

Having to make all transfers manually through checks or going physically to pay utility bills can be a hassle in the city’s fast-paced daily lives. This can be especially true if you own a business. Merchants have to send and receive payments to and from multiple entities, and some of them are recurring payments that have to be paid at the end of each month. ACH payments are more common than an average person may think. Many people are already involved in ACH transactions and are entirely unaware of it. An excellent example of ACH transfers is that most Americans receive their salary each month. It is automatically deposited in their accounts without fail each time. ACH processing works in various ways, from ensuring the security of the payments to timely recurring payments. ACH transactions can be much more efficient than writing checks and can be more cost-effective than paying with a credit or debit card.

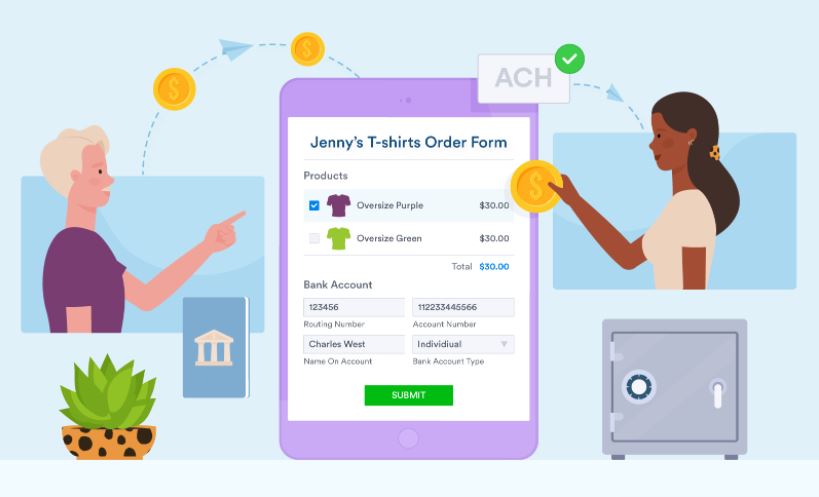

What is ACH?

The term ACH stands for Automated Clearing House. ACH is a type of online inter-bank transfer of funds that remains in a clearinghouse until the transaction’s authenticity is confirmed. Then it is sent to the receiving account of the transfer. Payments are processed in a batch to speed things up, which happens three times every business day. There are three main types of ACH transfers; direct deposits, direct costs, and split deposits.

Direct Deposits

When funds are transferred into a consumer’s account through a business or government source, it is classified as a direct deposit. These funds are transferred electronically to the consumer’s account on account of salary or any other funds due at the receiver’s end. These payments include reimbursed employer expenses, interest payments, paychecks, benefits by the government, and refunds in tax. If an amount is called a direct deposit, it’s at the receiving end.

Direct Payment

This payment method is used by businesses, government institutions, and even individuals to send money to an account. An example of his is the online bill payment method. Essentially, what you are doing is to send the money to the government using ACH. Also, payment apps that work more socially make use of ACH to allow the users to transfer funds.

By conducting an ACH payment, senders can see immediate debit in the sender’s account. Later, the amount is credited to the receiver’s account. Senders can see the debit with the transaction details, such as to whom the amount was sent and what the amount was. This is also called ‘pushing’ money from an account. The person receiving the amount sees it in their account as ACH credit. This is called ‘pulling’ money into the account.

Split Deposit

This is a way through which saving money for an individual becomes easier. This method helps to get automatic savings and control over one’s earning. Employees receiving a direct deposit can set a fixed amount that has to be saved. The amount to be saved is deposited into a savings account. In contrast, the rest of the amount is deposited in the employee’s primary deposit account. This allows workers to reach their short and long-term saving goals with better efficiency.

Benefits of ACH Payments

The most significant upside to ACH transfers is that they allow tracking funds and cash flow easily. This saves a business a lot of time and money in the long run. This can be especially helpful in tracking charges due to recurring billing. ACH processing is free for the people receiving the money, so they are much more desirable than wire transfers. Standard credit card processing can become very expensive because of the interchange fees and merchant services providers’ fees. Each time you swipe, dip, or key in a card through credit card processing, you will have to pay the fees for that transaction.

On the other hand, ACH processors charge 1% per transaction to businesses. This does not consider the size of the transaction; it can be as little or as big as the merchant desires. Therefore, keeping track of the money that you should have in your account and you will save on processing fees as well.

ACH processing is much easier to set up for customers. All someone needs to have is their customer’s banking information to send or receive funds. The customer’s banking information has to be entered only once into your system; after that, you can bill them recurrently. Customers will not be bothered by each payment as it will be deducted automatically from their accounts. Furthermore, you will not have to worry about attempted frauds. As credit cards have an expiry date, leaving you following your customers to pay for their purchase. The customer’s banking information is likely to remain the same for a very long time, so it won’t be the same with ACH.

Is it Really Worth It?

All you need to do to see how much you can save by ACH is to do a little math. While adding up the interchange and merchant account fees and comparing them with the meager 1% charged on ACH processing, you will be astounded to see the difference it makes. Also, businesses that don’t charge a lot per transaction or have lower monthly sales. The surety that only 1% of the transaction has to be paid in fees without any flat rate puts a small business owner at the same economic benefit as a bigger business owner. Let us give you a small example.

On average, processing with most credit card associations costs a merchant around 2.9%+.30¢ per transaction. Assuming a business bill each of their clients $5000 per month and has 25 clients. This can cost you around $1400 per month. With ACH, the same bill would average about merely $250-400 with most ACH processors. The business will be saving itself roughly $1100-1000 per month and more than $12000 a year! Another benefit of ACH transactions is that they are almost as hassle-free for the merchant as they are for the customers. Most Merchant services providers already provide ACH processing. All you have to do is look at their terms for you to accept ACH payments and begin!

{kind=link}